1. From Breakout Narrative to Reality Check

In my previous article from December 19, 2025, I outlined why 2026 marks the breakout phase for real-world asset (RWA) tokenization. At the time, the narrative was clear: tokenization had moved beyond experimentation and was entering production scale.

The numbers supported this shift:

- ~$30B RWAs on-chain (actuals)

- ~$9T forecast by 2030 (BCG / Chainalysis)

- Real estate among the top 3 fastest-growing segments, with projections of

👉 ~$1.4T by 2026 (Venturebloxx)

Additional industry forecasts point in the same direction:

Deloitte expects tokenized real estate to reach multi-trillion scale over the next decade

At the same time, industry narratives often reference already material market sizes — for example:

Zoniqx cites >$10B tokenized real estate in 2025, albeit without transparent methodology

The narrative is compelling – But narratives scale faster than markets.

2. A Simple Question — How Much Real Estate Is Actually Tokenized Today?

The term “tokenized” suggests something inherently transparent, traceable and measurable on a blockchain.

In reality, this assumption only partially holds.

Let’s start with what we can observe:

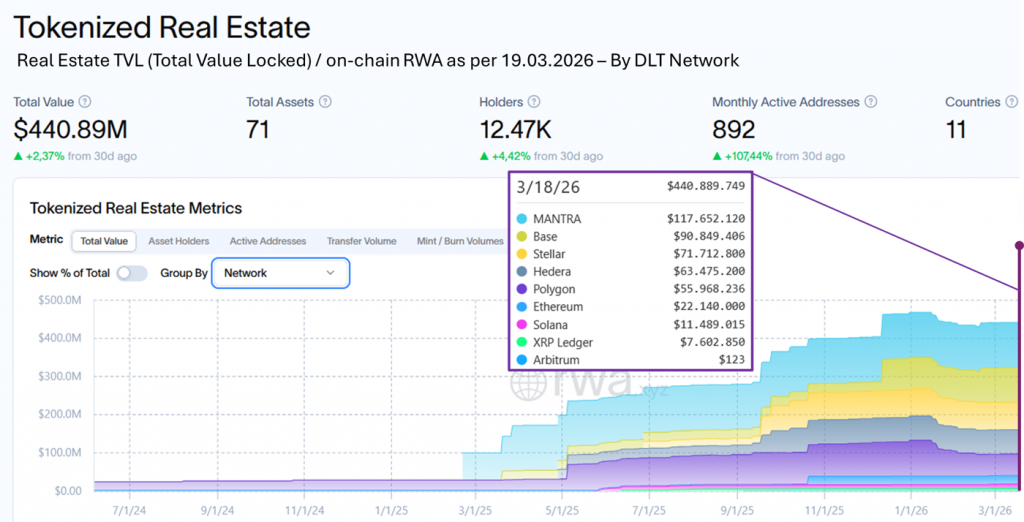

👉 ~$440M tokenized real estate on-chain (Q1 2026, RWA.xyz)

(see chart above – source: RWA.xyz)

This creates an immediate tension:

- $0.4B observable reality versus

- ~$10B commonly cited market size

Both numbers circulate in the same discussions — yet they seem fundamentally incompatible.

3. The Measurement Problem — Why Both Numbers Are “Correct”

The resolution lies in a simple but critical distinction:

Visibility ≠ existence

On-chain data captures only what is:

- publicly issued

- externally traceable

- technically indexable

Everything else — and that is most of the market — remains outside this lens.

To make sense of this, the market needs to be understood in layers:

🎯 Real Estate RWA Market Structure (Q1 2026)

🟢 On-chain (measurable / indexable)

Clarification:

Strictly speaking, “on-chain” would imply that legal ownership itself is natively represented by the token. In real estate, this is almost never the case due to land registries.

👉 Here, “on-chain / TVL” refers to publicly visible tokenized exposure, not legal title representation.

Definition:

Assets with public tokens and observable on-chain activity

Characteristics:

- Public chains (Ethereum, Polygon, Base, Stellar)

- Standardized tokens (ERC-20 etc.)

- Wallets and transfers externally visible

- Partial liquidity

Structures:

- Tokenized SPV equity

- Fractional ownership

- On-chain debt / yield products

Examples:

- RealT

- REENTAL

- Dubai (selected World Islands assets)

👉 ~$0.2B – $0.5B

🔵 Semi-on-chain (hybrid, partially visible)

Definition:

Tokens exist on-chain, but ownership and transferability are only partially observable

Characteristics:

- Custody layers (e.g. Fireblocks)

- Whitelisting / transfer restrictions

- Limited liquidity

- Investor mapping off-chain

Structures:

- Tokenized funds with restricted trading

- KYC-gated SPV equity

- institutional pilots on public chains

Examples:

- Securitize (selected real estate structures)

- U.S. private placement token offerings

- hybrid Dubai / Middle East setups

👉 Not reliably quantifiable

🔵 Off-chain dominated (not measurable / not indexable)

Definition:

Tokenization exists, but no meaningful public blockchain visibility

Characteristics:

- Custodian-held assets

- Private / permissioned systems

- SPV register as source of truth

- minimal or no on-chain activity

Structures:

- Institutional real estate funds

- private placements / club deals

- bank-driven tokenization

Examples:

- Securitize (core business)

- ADDX (Singapore)

- SDX (Switzerland)

- tZERO, BrickMark, SolidBlock

👉 Total market (incl. above): ~ $10B range

4. Resolving the Contradiction

The apparent contradiction dissolves once the layers are understood:

- On-chain data = observable surface (~$400M)

- Actual market = largely hidden (~$10B)

Tokenized does not mean observable.

This is the central misconception in today’s market discourse.

5. Reality Check on Forecasts

This perspective reframes earlier projections.

Scaling from ~$10B today to $1.4T by 2026 would require a level of adoption that is not yet visible in market structure, infrastructure, or deal flow.

👉 Near-term forecasts appear structurally overstated

The long-term thesis remains intact — but timelines matter.

6. Momentum Is Real — Even If the Numbers Lag

Despite this, the market is clearly moving.

In my day-to-day work with clients, prospects and partners, I see this shift very directly:

- I see institutional interest translating into concrete mandates

- I see increasing demand for tokenized capital formation structures

- I see more real-world implementations moving beyond pilot phase

- And most importantly, I see a clear rise in actual client projects

From an operating perspective, the shift is unmistakable:

Tokenization is no longer a concept — it is becoming repeatable business.

7. Conclusion — A Market Between Visibility and Reality

The real estate tokenization market today exists in two parallel states:

- Visible on-chain → small (~$400M)

- Economically real → significantly larger (~$10B)

Understanding this gap is critical. Because the future of tokenization will not be driven by:

- what is visible today

- or what is forecasted

But by how quickly invisible structures become scalable, standardized and integrated into capital markets.

Final takeaway:

The biggest gap in real estate tokenization is not growth — it is visibility.

And that is exactly what defines how early this market still is.